Private Real Estate Opportunities in an Era of Rising Interest Rates

Higher-for-longer borrowing costs are piling pressure on some sectors of commercial real estate, such as urban offices and retail outlets, already hard-hit by long-term negative trends. Other sectors, such as residential retail, are thriving. Seeking opinion from seasoned professionals is thus vital in assessing which of the emerging investment opportunities to participate in.

The US Federal Reserve held interest rates steady in September but signalled that it believes it can keep them high for quite a while yet, to bear down on inflation without causing a significant slowdown or large job losses. The same trend can be seen on the other side of the Atlantic, where the European Central Bank said in September that borrowing costs may have reached their peak but will remain high for as long as it takes to curb inflation.

That marks a sharp turnaround from just a few months back, when many investors believed that, as growth and inflation slowed, interest rates would fall back to the very low levels which markets had become accustomed to since the outbreak of the global financial crisis back in 2008. The sea change in interest-rate expectations and borrowing costs could reverberate across financial markets in general.

In real estate, higher financing costs, along with tighter lending standards, have already added some upward pressure on capitalisation rates and downward pressure on property values. Moreover, loans to develop real estate are harder to come by. The Wall Street Journal recently reported that US banks more than doubled their indirect real-estate exposure between 2015 and 2022. Now many are pulling back from the sector as valuations fall. The newspaper adds that lenders such as private debt funds, mortgage REITs and bond investors can also provide funding, but many of them are financed by banks and can’t get loans.[i]

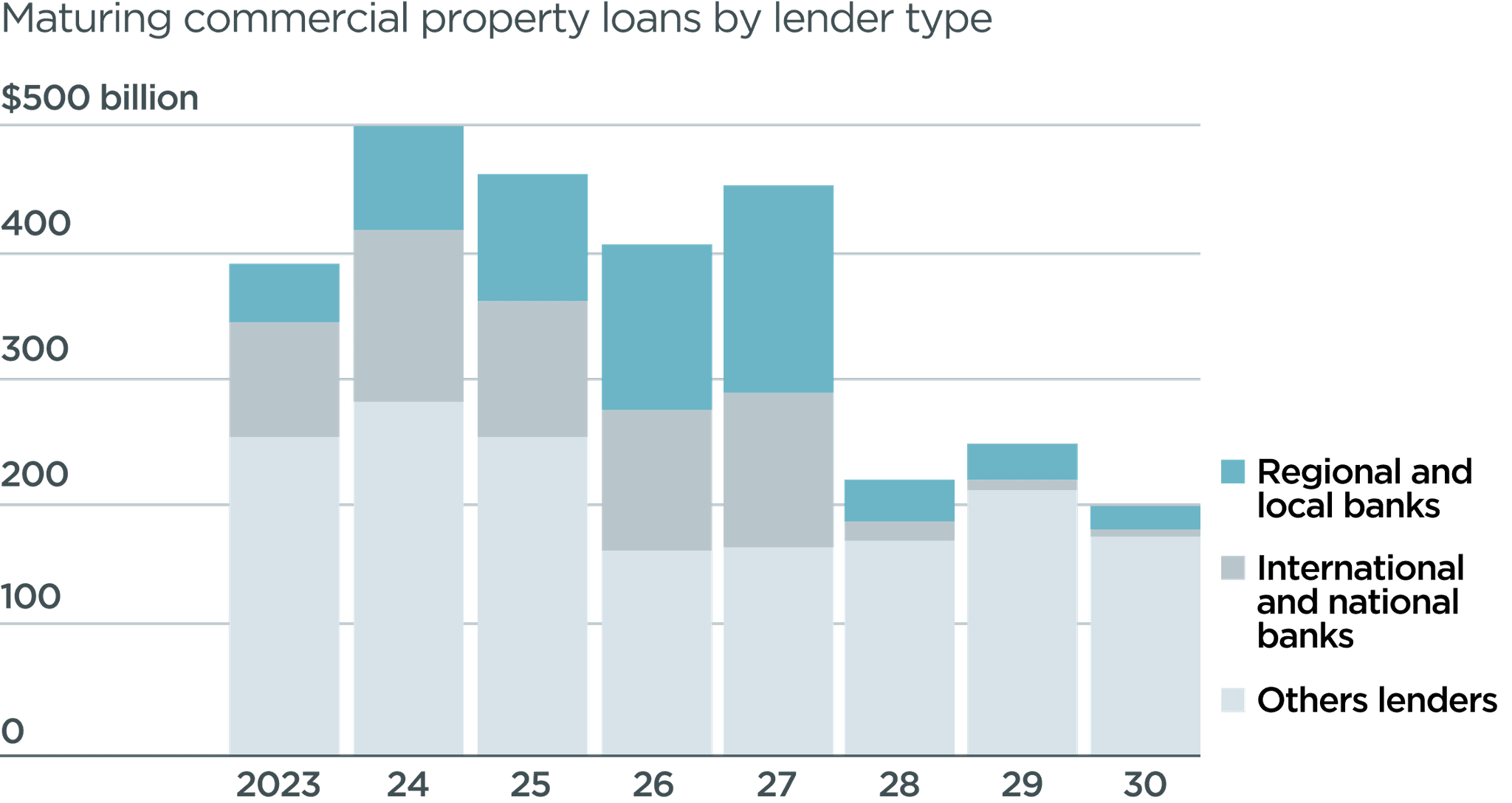

Moreover, around $900 billion worth of US real-estate loans and securities, most with rates far lower than those prevailing currently, need to be paid off or refinanced by the end of 2024. That will force many landlords to seek out more expensive financing from private investors and banks still willing to lend, or sell up, creating opportunities for cash-rich investors.

Figure 1: Maturing commercial property loans by lender type

The varying fortunes of real-estate sectors

Adding to the sector’s problems, secular trends are challenging some areas. Many city centres have yet to recover from the trend towards home working, shopping online and the migration to non-traditional urban areas accelerated by the pandemic. Indeed, some believe they never will. Fortune magazine recently reported that office vacancy rates in New York City have risen by over 70% since 2019. Meanwhile, Chicago’s magnificent Mile, a stretch of high-end shops and restaurants, had a 26% vacancy rate in spring 2023.

It’s a similar story in Europe. London’s office market, for example, has been bifurcated since last year. Older properties in less attractive locations have been increasingly facing vacating tenants, with newly refurbished or newly built product in the West End Core market enjoying steady occupancy and higher rents. The intra-sector mismatch has been accelerated with the push towards ESG friendly, sustainable assets, with tenants preferring those over old vintage space amid the constant regulatory push towards less carbon emissions.

The downturn in the office sector stands in stark contrast to surging demand and rents in many residential rental markets, where booming demand has far overshot chronically low supply. In August, the average annual rise in the cost of a rental property in London exceeded 17%.[ii] This year, New York has seen some of the highest increases in a decade, as inflation and rising expenses for property owners continue to aggravate the city’s affordability problems.

Amid all the doom and gloom in certain sectors of the market, the Wall Street Journal reports that Wall Street is raising funds to scoop up properties, many of which “will likely be sold at well below their recent prices, potentially triggering losses for owners and lenders”.

At Petiole we believe that, as ever, there are opportunities to be found amid distressed markets. Well located, sustainable, long-term let assets will continue to attract investor interest, while older assets with obsolescence risk in unfavoured sectors will suffer disproportionately.

Partnering with experienced investment professionals can be a game-changer in navigating these complex real-estate markets. These professionals can provide invaluable insights, access to data, and expertise that save investors both time and effort. Collaborating with seasoned professionals is a prudent strategy to capitalise on the emerging opportunities in the commercial real-estate sector.

Key takeaways

Higher interest rates are likely to be here for much longer than many investors – and borrowers – expected, with far-reaching implications for financial markets.

Commercial real estate is one of the most vulnerable areas, its vulnerability exacerbated by the secular winds blowing through some sectors, such as the office market.

However, that also means opportunities will emerge for long-term investors. The key is to partner with seasoned professionals who can identify true areas of value.

Disclaimer

The statements and data in this publication have been compiled by Petiole Asset Management AG to the best of its knowledge for informational and marketing purposes only. This publication constitutes neither a solicitation nor an offer or recommendation to buy or sell any investment instruments or to engage in any other transactions. It also does not constitute advice on legal, tax or other matters. The information contained in this publication should not be considered as a personal recommendation and does not consider the investment objectives or strategies or the financial situation or needs of any particular person. It is based on numerous assumptions. Different assumptions may lead to materially different results. All information and opinions contained in this publication have been obtained from sources believed to be reliable and credible. Petiole Asset Management AG and its employees disclaim any liability for incorrect or incomplete information as well as losses or lost profits that may arise from the use of information and the consideration of opinions.

A performance or positive return on an investment is no guarantee for performances and a positive return in the future. Likewise, exchange rate fluctuations may have a negative impact on the performance, value or return of financial instruments. All information and opinions as well as stated forecasts, assessments and market prices are current only at the time of preparation of this publication and may change at any time without notice.

Duplication or reproduction of this publication, in whole or in part, is not permitted without the prior written consent of Petiole Asset Management AG is not permitted. Unless otherwise agreed in writing, any distribution and transmission of this publication material to third parties is prohibited. Petiole Asset Management AG accepts no liability for claims or actions by third parties arising from the use or distribution of this publication. The distribution of this publication may only take place within the framework of the legislation applicable to it. It is not intended for individuals abroad who are not permitted access to such publications due to the legal system of their country of domicile.