Hanging in the Balance: Reasons for Caution Amid Market Euphoria

The past two years of stock market growth have been undoubtedly impressive, with the S&P 500 growing by 24% and 23% each year respectively. [1] The last time the market saw such outperformance was the mid-1990s, when the index enjoyed a stellar five-year period of uninterrupted growth of above 20% per annum. [2]

At this rate, one might think, simply leaving one’s money in a stock index fund is a no-brainer. But is such past growth truly sustainable?

A Closer Look at the Numbers

Markets initially rebounded from a troubled 2022, marred by concerns about global trade and politics. Since then, strong economic growth and steadily falling inflation have added to investor confidence.

If we look at the chart of the S&P 500 index over the past century, we can see that growth periods have typically been followed by flat periods lasting 10-20 years in length. The term ‘flat’ conceals the fact that such periods often included dramatic drawdowns of up to 50%, creating a very bumpy ride for investors in the process.

Analysts often turn to the so-called CAPE (Cyclically Adjusted Price-to-Earnings) ratio, developed by Robert Shiller, to assess whether valuations have reached excessive levels. The index compares stock prices to underlying earnings to identify if there is a gap between what investors are getting and what they are paying for. Shown below is the CAPE indicating high or low valuations for the S&P500 since the 1870s.

The CAPE currently sits at 36.98 as of January 2025, which is high by historical standards—close to the peak of the 2021 bubble (38.53) and more than double the pre-1990 average of 14.1. In fact, this level ranks as the third-highest valuation in the CAPE’s 150+ year history, underscoring how dramatically asset prices and underlying earnings have diverged over the past three decades.

Commentators are quick to point out that the CAPE is far from being an unerring guide to upcoming stock market corrections and crashes.[3] In support of the current high levels of optimism, bullish investors point to the rapidly accelerating prospects for AI or invoke concepts such as American exceptionalism.

Others argue that historical analysis of the CAPE is not entirely helpful, fundamental changes in the global economy (e.g. lower rates, more capital to be allocated) and the inability of book values to reflect intangible assets. However, it’s worth noting that many similar arguments were brought forward during the dot-com boom, before it became the dot-com bust and equity markets delivered flat returns for an entire decade.

Reasons for Caution

The Levkovich Index, maintained by Citigroup, indicated in December that investor sentiment had reached ‘euphoric’ levels, last seen in 2021.[4] This word should set alarm bells ringing for those familiar with market cycle theory.

Goldman Sachs is forecasting that the S&P 500 will see average annual growth of only 3% over the coming decade, and Bank of America is even less optimistic, forecasting growth of 0-1%.[5] Perhaps as worryingly, regulatory filings show that U.S. corporate executives are selling more stock than they buy.[6]

At the very least, it is possible that the market is due for volatility, if not a correction or a full-scale crash.

Overexposure to equities in such a scenario is dangerous for investors. A fall in value of 50% requires a rise in value of 100% in order to restore a stock to its former value. Furthermore, the psychological rollercoaster can induce either severe stress or worse, trigger irrational actions, such as selling on the downswing.

What’s the Alternative?

A good way to prepare for a potentially turbulent period in public markets is to increase one’s exposure to private markets—private equity, private credit and real estate.

As we’ve written about previously, these asset classes can help to reduce the volatility of a portfolio’s returns by diversifying risk, and offering the prospect of enhanced returns during a time of general market malaise.

Private equity investments have been found to historically outperform their public equity equivalents by 4% on average.[7] Private credit investments, meanwhile, have been shown not only to deliver higher returns but also lower volatility[8], with some studies showing the latter to be roughly half that of public comparables.[9]

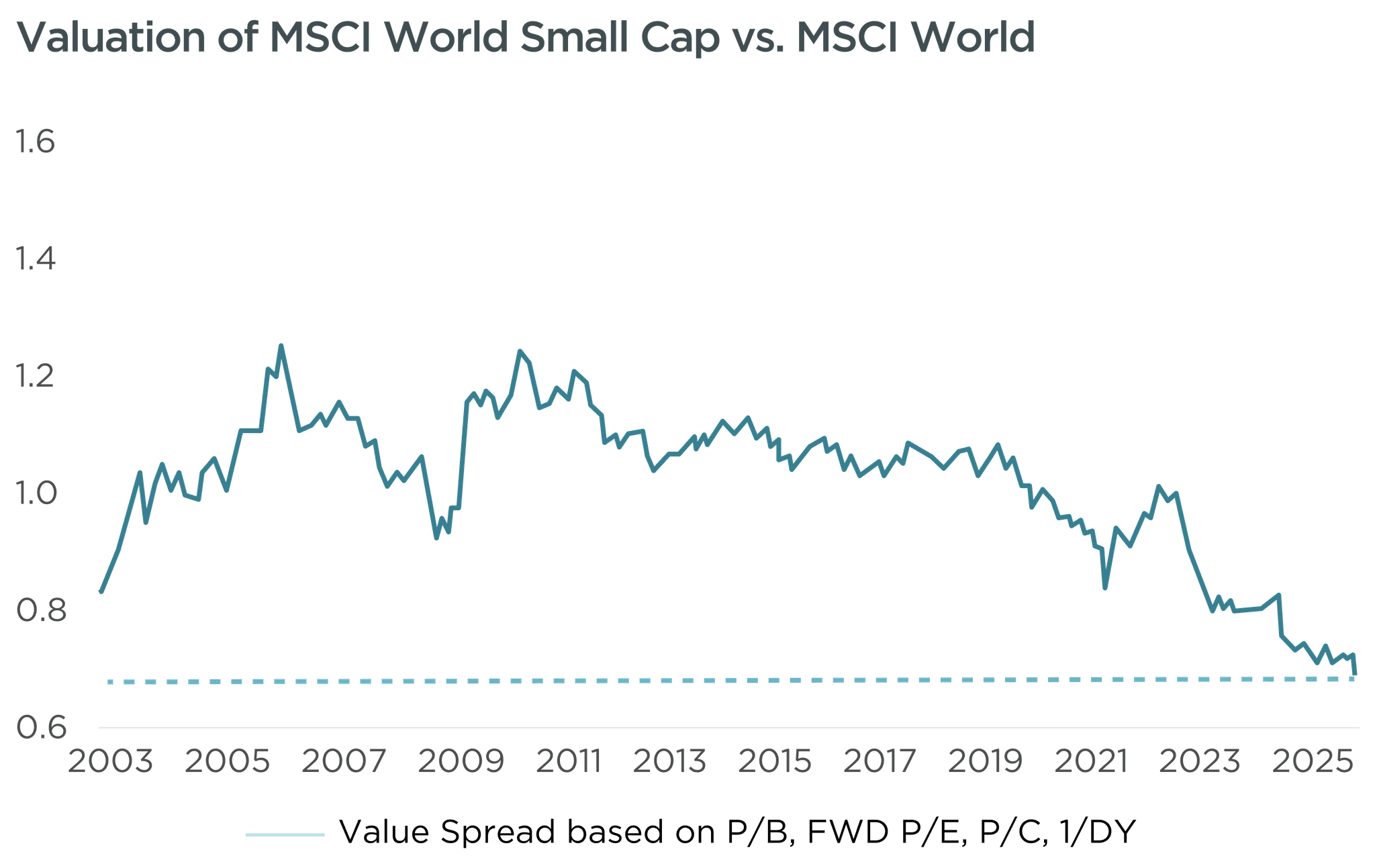

Another way of looking at the issue is by company size. Private investments are often (though not always) made in smaller-sized companies, which in recent years have increasingly outperformed larger companies, which have more distance to fall during times of turbulence (see chart below).

Conclusion

The right time to act in investing is almost always before the ‘right time’ actually arrives. Now, while markets are euphoric and bullish commentators are busy constructing arguments that this time is really different, wise investors will be quietly preparing their portfolios for what could be a coming storm. This can be achieved by divesting away from expensive (tech) stocks traded on the exchange and into smaller, more favorably valued companies—such as those found in private equity portfolios.

We are well-placed to assist our clients in diversifying their investments, as we have over two decades of experience successfully identifying and managing private markets opportunities. If you would like to discuss what this might look like for your portfolio, feel free to get in touch with one of our advisers.

This time may indeed be different. But would you stake your future on it?